Break out or Fake out?

All,

Those of you who have stared down the urea producers have improved your spread management position.

As you can see, we are clearly into the green. Is it a victory? LET’S DO THE MATH

Forward contracts for CZ23 have dropped about 50 cents per bushel since July 2022. If you use 150 bushel/acre as a base then you are down $75/acre on the sale of your corn, but you have saved $20/acre on your N cost….so a net opportunity cost of negative $55/acre.

I think this highlights the importance of grain marketing and not strictly focusing on your input costs…..as you purchase inputs it is wise to make forward sales. Yes, it feels good to see the spread back into the green but if at the same time corn coming down is the main factor for the relationship to fall into the green is it really a win? CLEARLY NO!

Now, above example just looks at one input, if we take a broader view of the overall crop nutrient market what does that look like?….after all, we are keeping score of the whole game not just one inning.

Here is the MATH considering the 4 macro inputs (N-P-K-S) priced on July of 2022 vs March of 2023.

Corn - $75/acre

Urea + $20/acre

Map + $6/acre

Potash + $9/acre

Sulfur + $8/acre

-$75/acre vs + $43/acre

Obviously, this is just a part of the bigger picture, you still have the big rabbits like labor cost, land, and machinery costs…etc. But it clearly emphasizes grain marketing importance. MAC always recommends managing spreads in proper proportions. If you lock in part of your inputs, it is wise to consider that proportion of your total cost structure and market outputs accordingly.

We are spread managers!

Let’s look at the charts because a picture is worth a thousand words. Remember, the main function of these charts is to signal the relationship over a long period of time and to give you confidence that the relationship is in your favor or not. It is not the only factor in profitability.

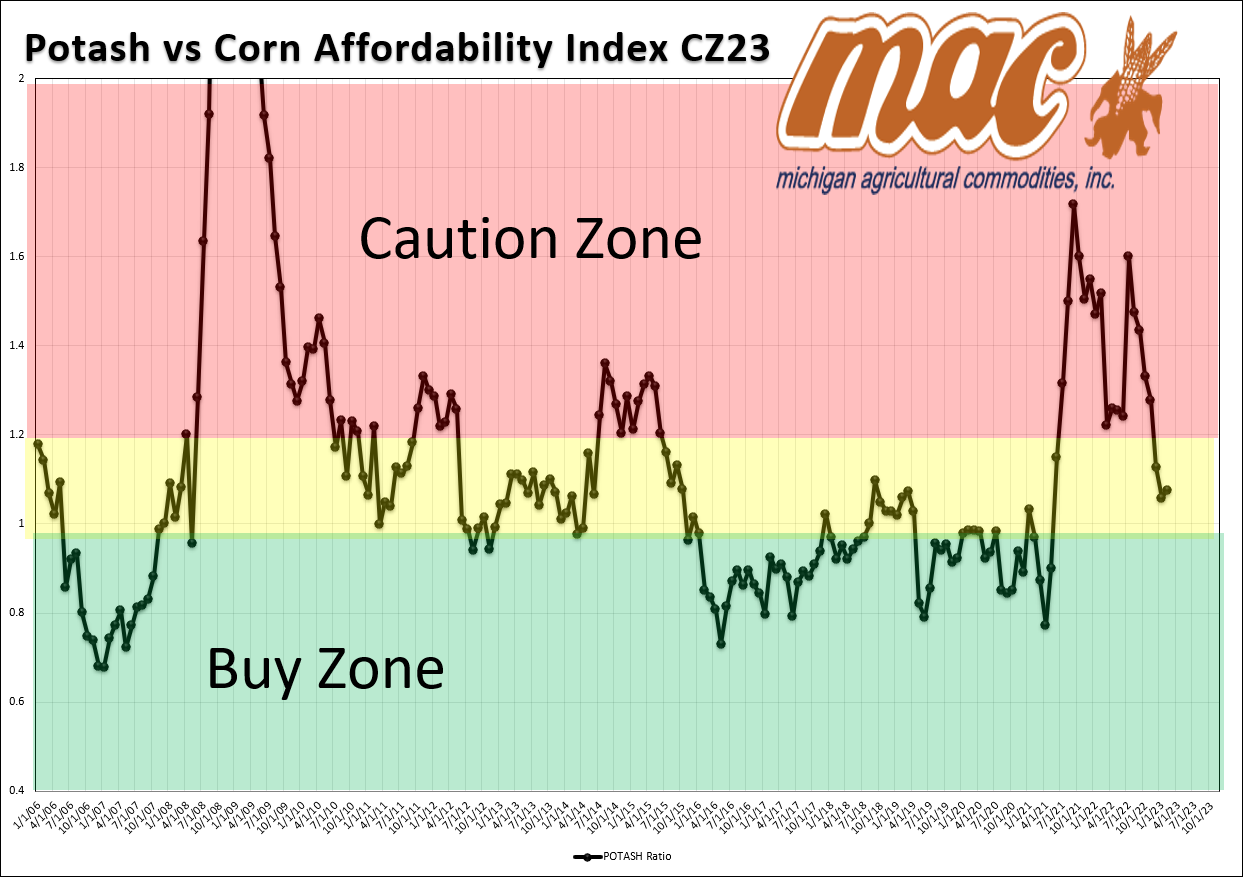

Potash

Potash may have found support here for spring pricing. It appears to me that most of the industry has taken a position to prepare for spring planting and I would guess that pricing will be sticky in the current range. $525-$600/ton

Some guys use these charts on P an K to signal when to build soil levels, when to maintain levels, and when to mine levels.

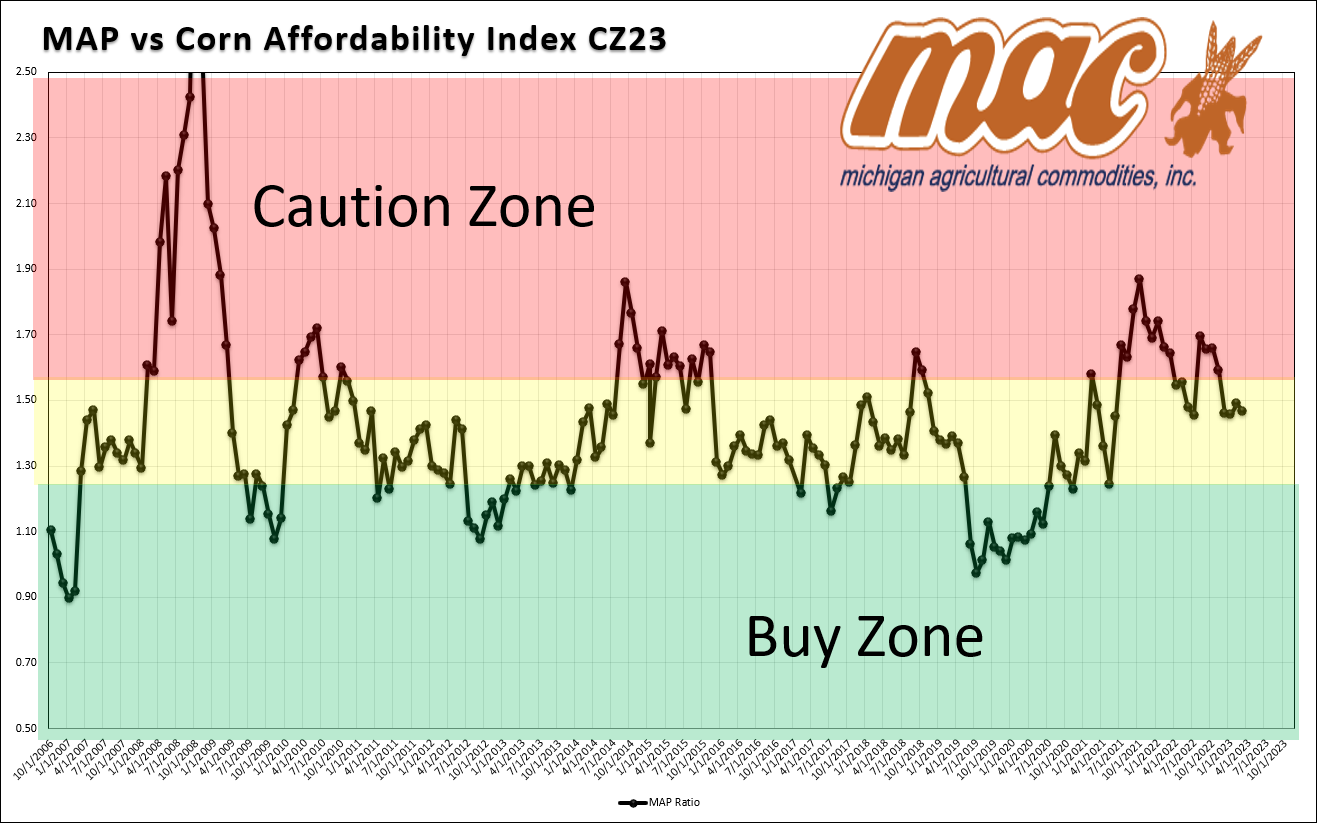

Phosphate

Of the four major inputs Phosphates seem to be holding up the best.

I think this value will fade thru spring. Expect 700-775 to be the starting price and it would not surprise me to see mid 600 by the end of the spring.

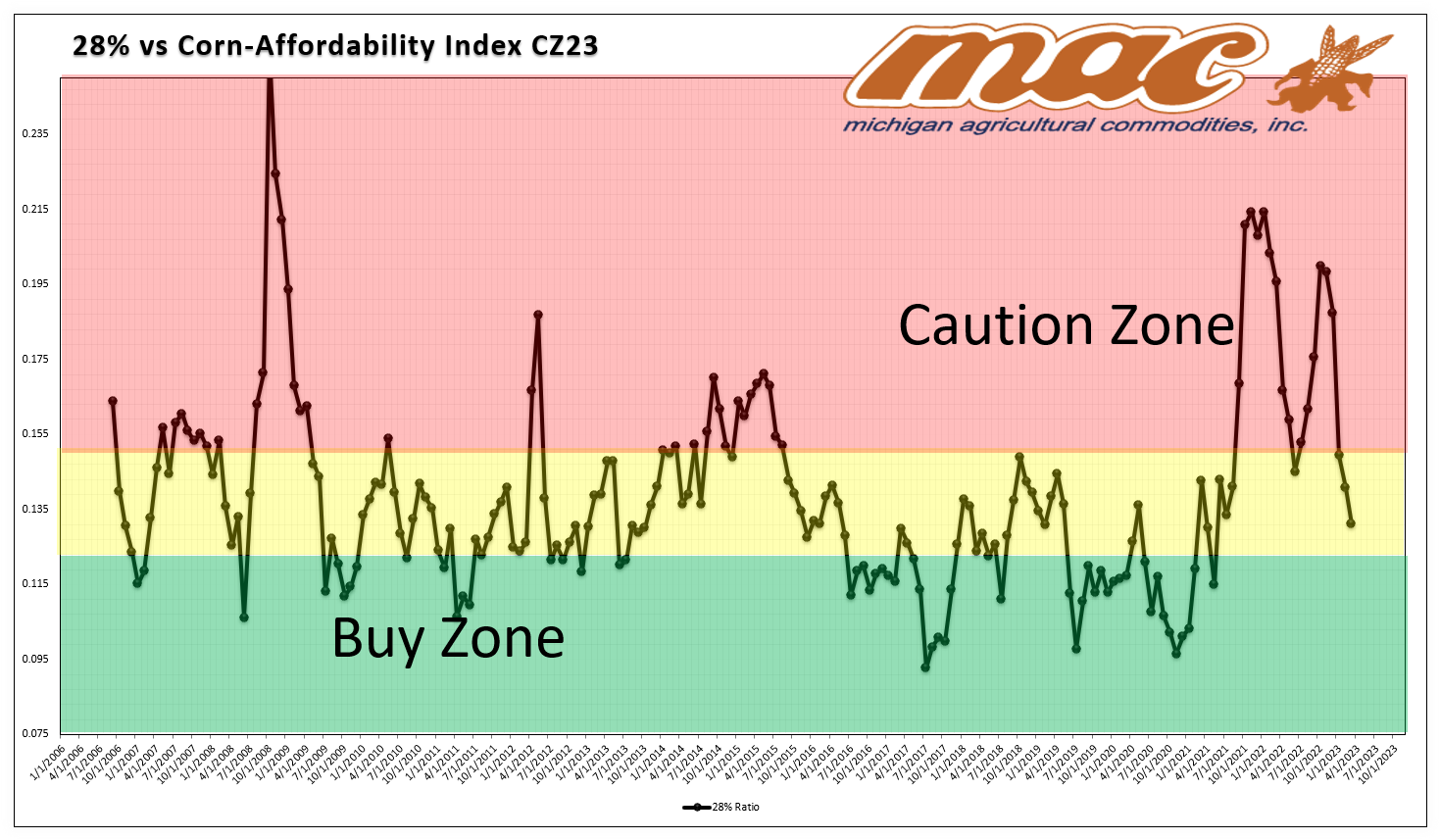

28%

CF and Koch have been pressured by imports since the turn of the new year. The summer fill values of last July have been taken out to the downside. A lot of suppliers have higher inventory values that will be lagging the spot market as it moves lower. I think the domestic manufacturers will be surprised at the amount of UAN that was purchased from abroad, and the spring spot volumes will be down more than expected. This could lead to a dismal summer fill program….remember we all have one-year memories. If corn moves lower….it will be even worse.

Add 9% cost of money to this equation and hold my beer. (ht- AB)

MACRO MINUTE

No geopolitics are mentioned here and there could be black swans that come to roost. The two I am keeping eye on are the war in Ukraine and the ongoing currency war. Weather is always an issue and will play its role somewhere in the world.

Known unknowns are not what usually burn you….unknown unknowns are what catch you with your marketing pants down!

Here is a long-term chart of corn that I think clearly lays out the downside and potential upside?.

US dollar strength/weakness will clearly play a roll in nominal value of corn. The chart below really clarifies inflation’s role in the price we receive. We are clearly near the upper end of the current price range.

Does your marketing plant have contingencies built in for a breakout? Or a test of support? Give your MAC merchant a call….we have programs to help on both fronts.

(KEY POINT HERE) Industry numbers from across the belt shows farms have sold half as much as they had sold a year ago to date. This is not an estimate…this is a fact!

Our one-year memories are signaling to us that we sold too soon last year, and we are not going to make the same mistake this year.

Making multi-year forward sales in 2008 and in 2012 were the right things to do(hindsight is 20/20) and 2022 may get added to that list. If the FED can bring inflation to heal and no black swans land, we will not breakout of the above “third level” and in fact, we may breakdown to $4 dollar support. (is that in your plan?)

I will leave you with this quote from the Chicago school of economics and 1976 Nobel Prize winner Milton Friedman.

Not sure of everyone’s take on this…but, printing 40% of the circulating supply of money in 24 months is not what I would consider “steady”. Somewhere between 2% and 40% lays the difference between Keynesian and Chicago schools of economics….LOL !

There are a lot of “ifs/ands/and buts” in above newsletter…”but” I wanted to draw out both arguments and highlight the risks we all face as an industry.

One of MAC’s goals is to help you be profitable in all economic environments. Managing risk will see us both thru to the other side of current market volatility.

Best Regards,

John Ezinga

C: 517-719-8200

VP-Agronomy

Michigan Agricultural Commodities, Inc.

PO 195 Middleton MI , 48856